LNG export in the US Gulf coast is a risky business. Alongside the human rights, climate and biodiversity impacts of the industry itself, the operation and expansion of methane gas1 liquefaction and its export infrastructure poses significant medium and long-term material financial risks to the investors, financiers and insurance companies involved.

As of early March 2026, the US-Israeli intervention in Iran and closure of the Strait of Hormuz have dramatically altered short-term LNG market dynamics. With QatarEnergy declaring force majeure on about 20 percent of global LNG supply,2 US LNG exporters stand to fill the gap at high prices and in turn capture extraordinary windfall profits—potentially $4 billion monthly in the near term, rising to $20 billion monthly if disruptions persist through summer.3 Operators with spot market exposure, like Venture Global (VG:NYSE), are particularly well-positioned to benefit.4

Yet, today’s windfall profits don’t change tomorrow’s structural risks.

Indeed, these crisis-driven windfalls underscore rather than contradict the financial risks in the sector. The LNG export business model as it is depends on volatile commodity markets and geopolitical instability—conditions that can reverse as quickly as they emerge. As discussed below, the same market forces delivering windfall profits today expose these highly-leveraged companies to severe downside when conditions normalize. What’s more, supply disruptions of this magnitude further damage the reputation of gas and LNG as a reliable and affordable fuel. Synthesizing the latest economic and financial research, this brief provides a synopsis of the market, legal, reputational and physical climate risks of US Gulf LNG export which together amount to significant, structural (and possibly underpriced) material risks. These risks will only be amplified if short-term excess war profits encourage even more aggressive expansion and even deeper company indebtedness. The brief examines the company Venture Global as an illustration of the financial risks undergirding the highly volatile and highly leveraged LNG export business model. The brief concludes with the financial risk management implications for actors currently supporting new LNG export terminal expansions.

US LNG Export Market Risks

US supply of LNG to global markets is booming. The current Middle East crisis has temporarily tightened global LNG markets, with US LNG exporters aiming to fill the supply gaps. However, the structural oversupply dynamics described below could very well reassert themselves once the crisis resolves—potentially with greater force if US exporters use windfall profits to accelerate expansion plans.

Meanwhile, medium-term demand growth remains highly uncertain. This supply-demand mismatch poses significant market and business risks across the supply chain but particularly for LNG exporters and their offtakers.5

Aggressive LNG supply rapidly producing a glut…

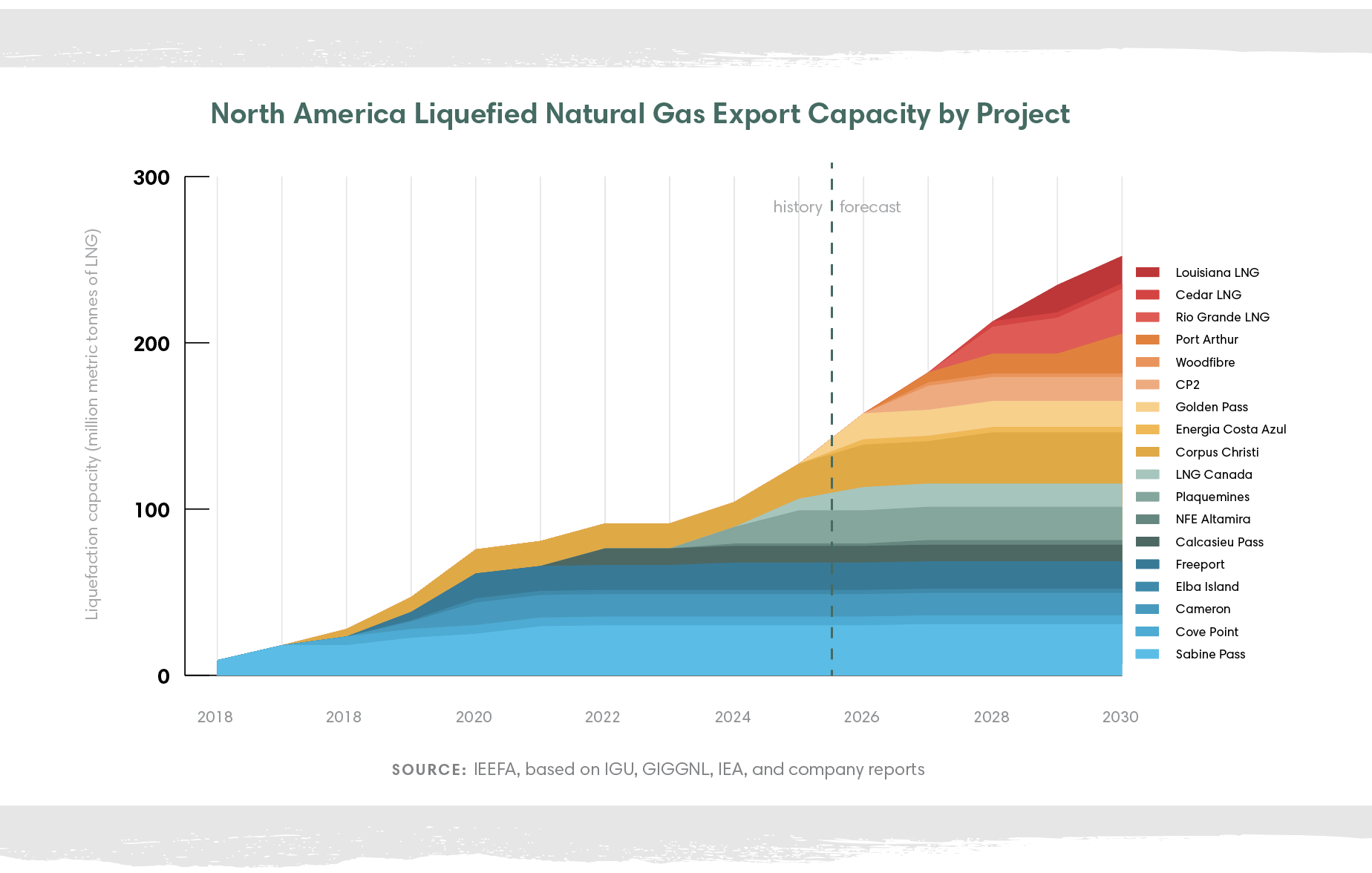

The United States leads the world in LNG expansion projects. If current trends continue, US export capacity will double by 2030, making the country the supplier of one third of the world’s liquefied methane gas.6 In 2025, final investment decisions (FIDs) backing new export terminals in the US Gulf South reached an all time high in the United States,7 with Venture Global’s CP2 LNG project securing a $15.1 billion FID, Rio Grande LNG (trains 4 and 5) securing $13.4 billion, and several other large projects following suit. 8

Fueled by US exports, industry analysts from S&P Global, the International Energy Agency (IEA), and the Institute for Energy Economics and Financial Analysis (IEEFA) have widely surmised that the worldwide LNG market is entering a period of oversupply.9 Global export capacity of the liquefied gas is expected to increase by 300 billion cubic meters by 2030.10 So many new terminals are coming online that supply may well outpace demand, in turn driving down prices.11 In contrast to previous waves of supply growth, more of this new supply (approximately 75%) does not have a set destination, either remaining uncontracted, or with a flexible destination contract clause.12 Contracts from LNG companies in the United States are known to be among the most flexible in the global market. In practice, this means that a period of low LNG prices could result in the U.S. LNG fleet being underutilised if buyers cancel their cargoes.13 It remains far from certain, in other words, that the market can absorb this supply surge. BloombergNEF forecasts supply exceeding demand between 2027 and 2030.14

The sheer volume of capacity under development,” said one industry expert late last year, “raises fundamental questions about market balance and the risk of prolonged oversupply.”15 Another analyst put it more bluntly: “there will definitely be an LNG glut.”16

…while sustained global LNG demand is wavering.

Like other commodity producers, the LNG export industry and its gas suppliers have in-built incentives to paint a rosy demand projection picture. Even if the demand isn’t there now, they assert, this new wave of supply will eventually stimulate a demand response. As more LNG comes online – the argument goes – the cost of the fuel in Europe and Asia will approach the marginal cost of supply in the U.S.17 This would mean higher prices for US households,18 but would trigger price-sensitive markets in Asia to absorb the cheaper gas, in turn limiting the risk of production shut-ins at LNG export terminals.

In contrast to the exporters’ bullish optimism, however, Goldman Sachs researchers – taking into account real-world constraints like limited gas storage capacity – “expect global LNG supply to increase by over 50% by 2030 vs 2024, a pace far faster than what we’ve observed for LNG demand growth in recent years.”19 Should supply outstrip demand this way, those supplying and trading LNG “will likely face an extended period of low prices and slim profits,” notes IEEFA.20

Lower prices mean tighter margins. Combine these tight margins with the high debt loads the LNG exporters are bearing (discussed below), and you have a growing risk of speculative excess driving overinvestment and serious credit and equity risks.. This is particularly the case for investors or creditors exposed to projects with high uncontracted capacity and merchant exposure.

Part of the question is whether LNG demand – particularly in Europe and Southeast Asia – will rise to meet the surge in supply from these aggressive and highly-leveraged LNG expansions. While there is some evidence for lower prices boosting near-term demand in some regions, four key factors present serious doubts about the sustainability of LNG market demand globally.

1. Dwindling demand in key markets, especially Europe, Japan & South Korea

Following the Russian invasion of Ukraine in 2022, European countries rapidly built gas import infrastructure to offset its dependence on its supplier to the East with a new dependence on expensive US gas importation.21 While EU gas imports from the US rose in 2025,22 Europe’s new LNG import infrastructure buildout slowed significantly last year, with multiple projects cancelled or shelved.23 IEA expects European gas demand reductions by 2% in 2026, driven by the continued expansion of renewables.24 Likewise, IEEFA projects that European LNG imports are likely to fall 20% between 2025 and 2030 as the region decarbonizes.25 A strong sense of energy self-determination is growing across the EU. Just this January, the EU Energy Commissioner Dan Jørgensen said, “we are not aiming at replacing one dependency with a new dependency. We want to grow our own energy and our strategy in the future is to become free of gas.”26 In 2025, Europe generated more electricity from wind and solar generated than fossil fuels for the first time, possibly heralding a new tipping point for energy security, sovereignty and affordability in the region.27

For their part, Japan and South Korea are almost entirely dependent on LNG to meet gas demand.28 Yet neither country is likely to be a source of significant future demand growth over the medium or long-term.29 In Japan, gas consumption has steadily declined from a peak in 2014, as nuclear restarts and renewables growth have offset the need for LNG in power generation.30 As a result of declining demand at home, Japan’s largest LNG buyers are increasingly aiming to resell more LNG volumes abroad, potentially exacerbating global oversupply.31 South Korea aims to cut the share of LNG in its power mix by 18% through 2038.32

2. Challenges to long-term demand growth in Southeast Asia from infrastructure delays, bankability, and economic challenges

Countries in Southeast Asia are seen by the industry as a major driver of global LNG demand.33 Across the region, optimistic projections about LNG development are being tempered by challenges surrounding regulation, bankability and equipment procurement.34 Infrastructure delays have posed challenges in Vietnam and the Philippines, for example. For demand to grow, infrastructure must be present to import, store, transport and use the fuel. The Philippines Secretary of Energy recently announced that the country is unlikely to add new import capacity amidst low utilization rates and serious gas turbine bottlenecks.35 Vietnam–whose wind and solar generation has increased by nearly 600% since 201936–is seeing similar delays in gas-fired power implementation, with gas turbine manufacturers reporting wait times of five years or more to obtain a turbine.37 High competition for gas power equipment from wealthy countries puts middle-income markets at a significant disadvantage.38 Infrastructure limitations and renewable deployment may ultimately put a cap on demand growth potential. Saturating the market with low-cost gas is far from a magic bullet in stimulating regional demand.

3. China’s energy strategy gives it a “wild card” status

China – the world’s largest LNG importer – is a “wild card” for LNG, according to the IEA’s most recent World Energy Outlook.39 The country’s LNG import declined steadily in 2025, as its own gas output picked up and it struck a gas pipeline deal with Russia.40 Early 2026 saw Chinese companies reselling shipments, which, according to Bloomberg, signals “that Asian demand remains weak, and LNG will flow to buyers willing to pay more.”41 The energy supply in China is diverse, with plenty of cheaper energy sources including domestic gas, pipeline imports from Russia, coal, and rapidly-growing renewable energy resources. Clean energy drove over a third of China’s GDP growth in 2025,42 while experts believe the country is well-positioned to accelerate its short-term energy transition.43 Investors are unsure if the country’s long term appetite for LNG will grow given these alternatives.44 In the scenario where China’s demand stagnates, it could seek to resell already-contracted LNG volumes, which would serve to accelerate the oncoming glut.45

4. Fast-growing adoption of renewables is beginning to crowd out LNG import

Surging adoption of cost-competitive renewable energy technology is the fourth critical factor likely to reduce secular demand for imported LNG globally. Evidence from power markets shows that renewables are already rapidly increasing their share of power production globally.46 Analysts from IEEFA suggest that this uptake of renewables is in direct competition with gas and may temper gas demands in several relevant markets.47 Under any of the IEA’s outlook scenarios, renewables are set to grow faster than any other major energy source, led by solar photovoltaics.48 In two of the three scenarios, renewable energy growth and electrification increasingly limit LNG demand growth, especially in Europe and China.49 European LNG buyers themselves anticipate a gradual decline in LNG demand through at least 2040 as renewable energy infrastructure expands across the continent.50

Again, these demand barriers cannot be easily resolved by flooding the global market with cheap LNG. Goldman Sachs argues that the combination of storage limitations and congestion pressures driving prices lower could make “US LNG exports uneconomic to flow” in 2028/29, potentially resulting in cancellation of US exports.51

Short-term LNG volatility cuts both ways

The current Persian Gulf crisis demonstrates the extreme volatility inherent in LNG markets. While US exporters may capture windfall profits of $870 million per week above pre-crisis baselines during the current disruption,52 this same volatility poses severe risks when conditions inevitably reverse. The 2022 Ukraine-driven rally delivered an estimated $84 billion in windfall profits to US LNG over 12 months53—yet was followed by the type of oversupply and margin compression detailed in this brief. As discussed below, highly-leveraged operators like Venture Global face acute risk from the inevitable reversion to normalized (or depressed) pricing. Crisis profits may encourage further indebtedness and further overexpansion, setting up even greater exposure when the next downturn arrives.

Passing the buck to LNG offtakers may not be a sustainable business strategy.

LNG exporters are well-aware of this fundamental demand uncertainty and associated market risk. Typically, liquefaction terminal owners like Venture Global and Cheniere address this by passing the risks to offtakers through longer-term Sales and Purchase Agreements (SPAs) which can offer owners fixed liquefaction fees on a take-or-pay basis — regardless of whether the fuel is taken by the buyer.54 This tends to send a signal of a durable demand horizon and secure revenues.

However, LNG exporters’ strategy to displace market risks onto LNG offtakers has its limits and could backfire on both parties. As noted above, the United States is the most flexible supplier of LNG and therefore is the most exposed to low LNG demand.55 Terminal owners are not always completely contracted and some, like Venture Global, rely at least in part on the spot market to sell uncontracted fuel.56 More fundamentally, contracts don’t guarantee revenue. If offtakers are exposed to high degrees of market stress, they could cancel or delay cargoes, dispute payments or even default.57 Furthermore, LNG buyers are increasing their interest in the short-term contract market, particularly in Southeast Asia where, in a 2025 survey, 77% of surveyed buyers expressed interest in buying on short-term contracts, an increase of 40% over 2023 survey results with a corresponding marked decline in buyers in the region wanting to pursue long-term contracts.58 Lastly, climate-driven extreme weather events have already forced operational stoppages, especially along the US Gulf South where LNG export is most concentrated.59

Material Climate Risks of LNG Export in the US Gulf South

In August, 2020, just weeks after the Cameron LNG terminal (jointly owned by Sempra, TotalEnergies Mitsui and Mitsubishi)60 had reached full capacity, Hurricane Laura made landfall with an 18 foot storm surge. Damage to the electrical and marine infrastructure around the Cameron LNG facility persisted, knocking some 12 Mtpa of liquified methane gas offline for several weeks.61 In 2024, meanwhile, Hurricane Beryl shut down one of the largest operational LNG plants in the U.S. – Freeport LNG – resulting in 3 weeks of operational losses.62

US methane gas export is heavily-concentrated along the Gulf Coast,63 with 13 billion cubic feet of LNG leaving the region every day.64 While the Gulf offers some geographic and cost advantages, the region is also one of the most exposed to the rising number and severity of extreme weather and climate-driven natural disasters, as discussed below.

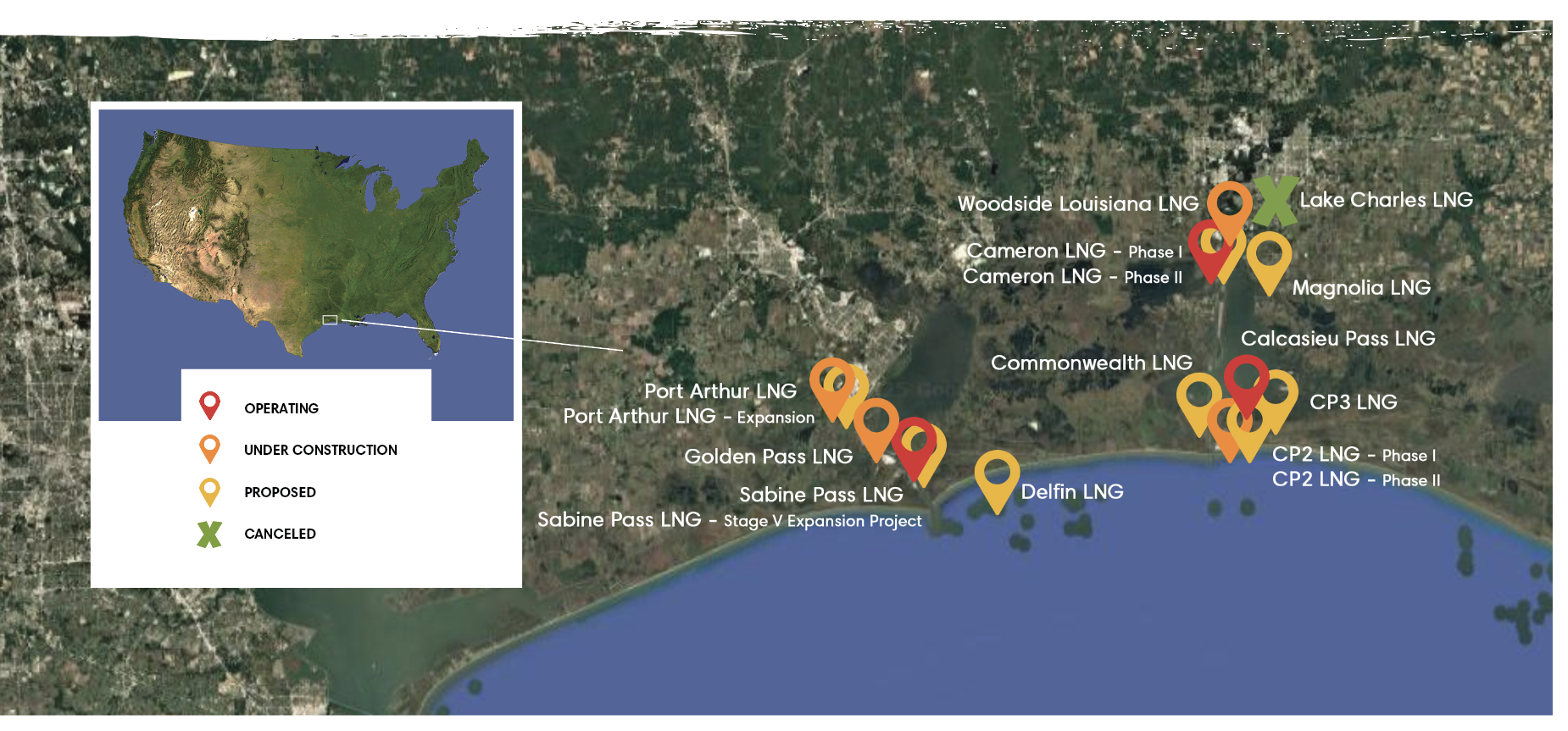

Increasingly intense hurricanes and associated storm surges are the most acute risk in the US Gulf. Louisiana alone accounts for 30% of the US counties most exposed to flooding risk today.65 Future hurricanes could be even more disruptive, as the LNG export build-out becomes more and more concentrated geographically. Sabine Pass LNG (operating, with a proposed expansion), Golden Pass LNG (under construction), and Port Arthur LNG (under construction), for example, are projects densely located along Sabine Lake on the Texas-Louisiana border.66 A future hurricane event could disrupt the 66 million tons per annum (Mtpa) peak throughput capacity concentrated in just that small area. That’s over 15 percent of the global LNG trade per year.67 An unexpected and lengthy disruption in operations would not only send a price shock through global gas markets.68 It would also cost the companies dearly in lost revenues.

LNG terminals along the US Gulf Coast also face more chronic physical risks from climate change. The region is experiencing the highest sea level rise rates in the contiguous U.S.69 LNG export relies on an intricate and interdependent processing and transport infrastructure. Much of this critical infrastructure is well within range of sea level rise, according to NOAA.70 Higher overall water levels from sea rise mean more destructive storm surges, more frequent and more intense flooding. This also means more land shrinkage in the vicinity of many of the operating and proposed export terminals.71

Together, the combined effects of intensifying hurricanes, storm surges, sea level rise and land shrinkage pose significant risks of extended disruptions of LNG export terminals. Retired US Army General Russel Honore has concluded that LNG plants are in a “hurricane disaster zone” and pose unacceptably high risks.72

Venture Global LNG Particularly Exposed to Market and Physical Climate Risks

Venture Global LNG has the largest expansion plans of any LNG exporter in the U.S.73 As discussed in more detail below, the company – in part due to its aggressive expansion, heavy reliance on debt, its unique business model and its geographic location – is particularly exposed to the market and climate risks haunting the sector.

Market Risks: Venture Global’s Business Model Exposes it to Significant Market Volatility

VG plans to cement itself as the biggest LNG developer and operator in North America, aiming for 100 Mtpa of LNG export capacity in operation or construction by 2030.74 Its export terminal portfolio consists of two operating LNG export facilities in Louisiana: Calcasieu Pass LNG and Plaquemines LNG.75 The Plaquemines facility alone accounted for over 60% of the increase in global LNG supply in 2025.76 VG is also constructing a third, CP2 LNG, whose Phase 1 reached final investment decision (FID) in 2025.77 On top of that, the company is planning a massive expansion at the Plaquemines LNG facility, the Phase 2 of CP2 LNG, and an additional terminal called CP3 LNG.78 These expansion plans have not yet reached FID.

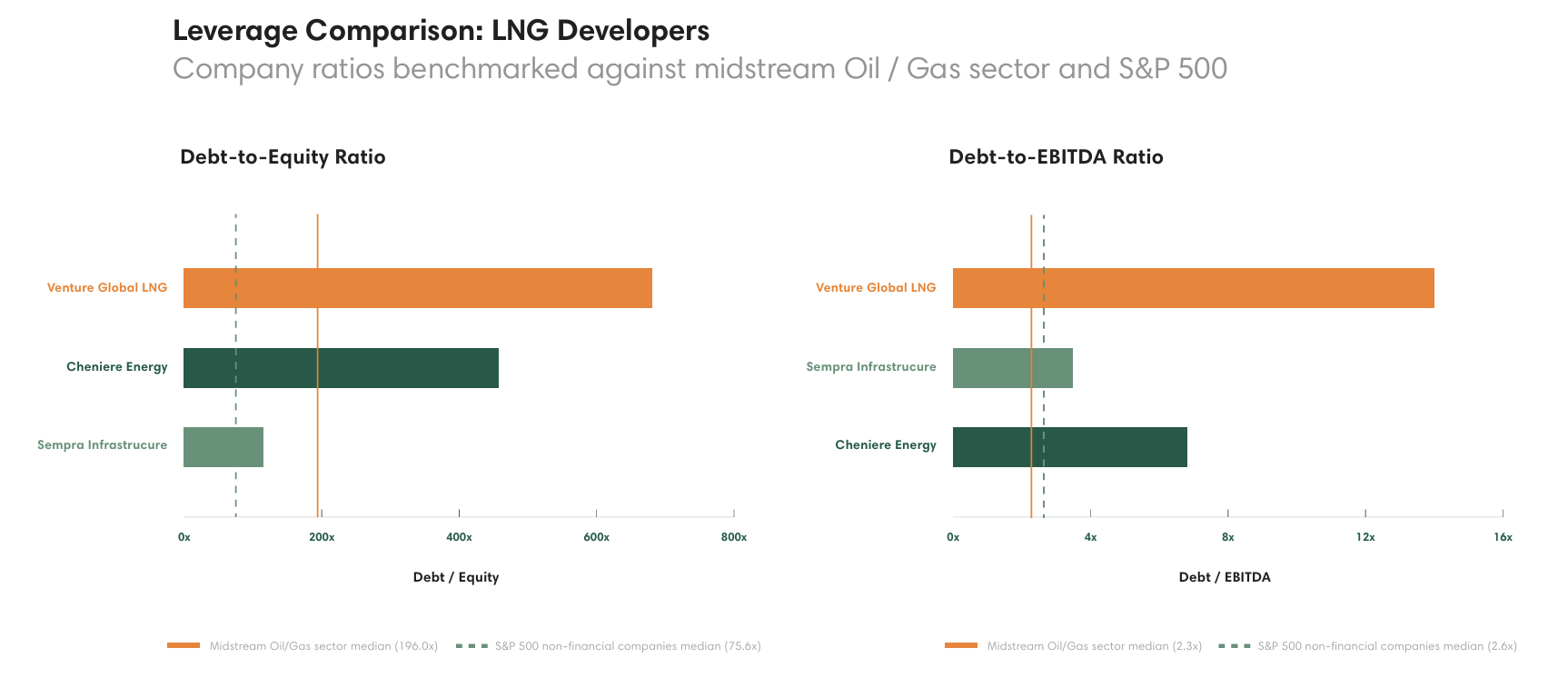

These aggressive expansion plans don’t come cheap. The company holds over $32 billion in debt raised mostly to finance these heavy capital investments.79 On every relevant measure of its leverage ratio (an often-used measure of a company’s ability to pay off its incurred debt), Venture Global’s debt load far surpasses its competitors as seen in the chart below.

Venture Global’s Leverage Ratios Compared80

Venture Global joins its peers in the region in holding significant debt. As of late 2025, four of the top pure-play LNG export terminal developers collectively held over $70 billion in debt raised to finance LNG infrastructure.81

To give banks confidence in providing large-scale financing, VG enters into Sales and Purchase Agreements (SPAs) with offtake companies, which aim to lock in a steady LNG demand at a long-term fixed rate. Where VG’s model differs from traditional LNG facilities is in the strategy surrounding their “commissioning period.” VG is attempting a market innovation by building their terminals with a modular design using prefabricated components offsite, which allows them to begin delivering LNG earlier than usual. This has the added financial benefit of enabling the company to sell LNG on the spot market before they start providing it to clients through SPAs. This has resulted in a much higher margin on uncontracted spot sales.82 For example, in Q3 2025, the company earned an average liquefaction fee of $6.79/MMBtu from spot cargoes sold at Plaquemines LNG, which is still in commissioning. During the same period, it earned an average of $1.97/MMBtu from contracted cargoes at Calcasieu Pass.83 One Bloomberg columnist summarized that this strategy is efficient not only as a matter of engineering and construction, but also “as a matter of financial engineering and contract construction.”84

Perhaps. But the strategy also brought heavy risk to the company. For one, the rapid expansion has required the company to take on high ratios of leverage, which means VG relies on much more debt than it does cash flow to fuel its expansion. Short term sales can be lucrative on the market upswings, but are less predictable and exposed to the downsides of market risk. This means that unforeseen project delays, operational disruptions, disputes with suppliers and offtakers, or market swings all pose particular risks to VG revenue streams.

Fitch Ratings notes that VG’s cash flow is considerably more reliant on these short-term sales than that of its leading competitor, Cheniere.85 Last year, this Big 3 credit rating agency found that about 75% of VG’s earnings between 2025 and 2029 is likely dependent on a combination of commissioning-phase revenue and sales on the spot markets. Only a quarter depends on contracted volumes, according to Fitch’s 2025 outlook.86 VG itself notes that “our ability to generate proceeds from sales of commissioning cargos is subject to significant uncertainty and volatility in such proceeds, given significant volatility in spot-market prices.”87 While useful to boost cash flows, this unique financial engineering strategy has also eroded confidence and prompted legal action by investors88 and major clients, as described below.

Litigation Risks: “Epic Feud” with Own Clients Leads to Expensive Arbitration

While developing the Calcasieu Pass terminal, VG signed long-term offtake contracts with large clients including Shell, BP, Edison, PGNiG (now Orlen), Repsol, and Galp.89 In the context of soaring LNG prices following Russia’s invasion of Ukraine, VG reportedly proceeded to sell LNG on spot markets at higher prices rather than to its contracted clients.90 VG argued that it was necessary to commission and test the facilities for a longer period of time than traditional LNG.91 In any event, VG was reportedly able to sell LNG cargoes at high-margin spot market prices during the onset of the Ukraine war, instead of shipping it to these clients with long-term and lower-margin contracts. The gains for VG were, by some estimates, in the billions of dollars.92

Some of its clients interpreted their contracts differently and filed seven separate arbitration proceedings.93In August 2025, Venture Global won its arbitration dispute against Shell and projected confidence that it would win similar disputes with the remaining clients.94 However, in October 2025, VG lost its case with BP, which is seeking damages ranging between $3.7 billion and $6.0 billion, as well as interest, costs and attorneys’ fees according to Venture Global.95 The International Chamber of Commerce tribunal ruled that VG had breached its contract obligations and failed to act as a “Reasonable and Prudent Operator.” A penalty will be determined in a hearing in 2026 or 2027.96

The fallout from these disputes has been significant. Venture Global’s stock fell almost 20% immediately following the BP loss.97 S&P and Fitch downgraded the LNG company’s outlook from ‘stable’ to ‘negative’ in October 2025.98 TotalEnergies publicly rejected the company as an LNG supplier, with the CEO saying, “I don’t want to deal with these guys, because of what they are doing. … I don’t want to be in the middle of a dispute with my friends, with Shell and BP.”99

Pending damages from the remaining arbitration could be vast, according to Venture Global’s own disclosures.100 In early 2026, VG stated that it had settled one proceeding with an un-named medium-term customer and an arbitration tribunal had ruled in its favor in a dispute with Spain’s Repsol in early 2026.101 Yet, damages for the remaining four cases could approach $10 billion if the remaining cases are decided in the clients’ favor. In addition to BP seeking up to $6.0 billion in damages, at least three other customers seem to have open arbitration cases pending in excess of $3.9 billion, according to Venture Global’s March 2026 annual disclosures.102

Further legal and reputational risks: Dredge fast and break things

Community opposition to VG projects is strong. Fishers have blamed the buildout of LNG in the region for hurting shrimp, fish oyster, and crab fisheries and are worried it will destroy their industries and economic livelihood.103 In August 2025, in an effort to prepare for the buildout of VG’s CP2 facility, contractors commissioned by VG and port authorities to widen shipping lanes through dredging as part of the CP2 site preparations spilled large amounts of dredging sludge into sensitive ecosystems in the vicinity.104 Affected fisherfolk found that the spill increased the rate of oyster deaths, hurting the already-imperiled seafood industry.105 They are seeking compensation for the loss of their catch and future losses, and have also joined local community members in voicing public protests,106 drawing attention to the issue and inviting reputation risk to Venture Global.

This dredging incident reflects a pattern. According to state and federal records reviewed by the Environmental Integrity Project, the company’s Calcasieu Pass LNG terminal has been out of compliance with the Clean Air Act for the entire duration of its commissioning and operation, at least from October 2022-July 2025. These records show that the terminal routinely releases pollutants, including over 900 tons of locally health-damaging pollutants and over 3 million tons of greenhouse gases in 2023. To date, settlement on these violations has not been reached.107 While pollution fines tend to be insignificant financially to multibillion dollar companies, a track record of violations can lead to courts blocking and revoking permits for existing and future expansion projects. For example, Commonwealth LNG, a project close to Venture’s Calcasieu Pass projects, recently had its permit revoked for failing to consider its effect on surrounding communities, as well as the project’s climate harms108 Following the dredging spill, local and national groups filed a motion in federal court seeking to halt construction of CP2, alleging that dredging activities violated permits and damaged fisheries.109 Reputational risks thus can quickly translate into material financial risks for LNG terminals.

Climate Risks: Venture Global operating in 2 of the top 10 most at risk counties in the US

In 2021, Hurricane Ida hit the area around Plaquemines Parish, flooding the low-lying site where VG’s Plaquemines LNG terminal would eventually be built.110 VG has attempted to mitigate these sorts of risks by constructing 26-foot seawalls on site. Yet, environmental scientists have pointed out that the facility lies at risk of being flooded or isolated from land by a large storm.111

Like other LNG terminals across the US Gulf Coast, Venture Global’s export facilities are facing increasing risks from climate-driven extreme weather. The company’s main operations in Cameron Parish and Plaquemines Parish each sit in areas heavily exposed to hurricanes, storm surges, sea level rise and land shrinkage, as explored below.

These are not isolated, freak incidents. Flooding risks in particular could render facilities across VG’s assets inoperable. Cameron Parish – where VG’s Calcasieu Pass (CP) LNG terminal is built – was ranked the #1 county in the US most at risk of the type of flooding that could lead to loss of operational functionality (“operational flooding risk”).112 96.4% of Cameron Parish’s physical infrastructure is already at risk of flooding today, and 100% of commercial properties face this operational risk.113 Plaquemines Parish – where VG has its other operating LNG export terminal – was ranked the #6 most at risk for operational flooding countrywide, with 85% of its infrastructure and 99.8% of its commercial properties at threat of damaging flooding.114

With its only physical assets concentrated in the two of the US’ top ten most at risk counties for flooding, Venture Global seems to be doubling down on sinking ground.

The company is building its second Calcasieu Pass LNG terminal alongside the same water front as its first Calcasieu Pass LNG terminal.115 The Plaquemines Phase II expansion under construction is also just adjacent to Phase I currently in operation. That is, the lion’s share of the company’s $50 billion in assets116 are densely concentrated in two of the country’s top 10 riskiest counties for climate-driven flood risks which could make business inoperable. A major storm could disable a substantial portion of VG’s capacity, leading to cargo delays and losses to the income the firm needs to service its high debt loads. If facilities fail, VG would incur expensive repair and replace costs and may face liability exposure. These losses could also potentially create lasting uncertainty about the company’s ability to honor its contracts.

Insurance companies across the country are already retreating from climate risk-prone areas across Louisiana.117 The average annual loss (AAL) data insurers use to understand risk at VG’s LNG facilities is not public. But increasing exposure to physical climate risk may lead insurers to increase premiums or even drop insurance policies the company currently has, as has happened to households across the region and the country.118 Already, Venture Global disclosed that it uses a captive insurance subsidiary to insure certain risks related to named windstorms like a tropical storm or hurricane.119 This approach, the company concedes, “involves retaining certain risks that might otherwise be covered by traditional insurance.”120 In other words, this heavily indebted company is – in part – insuring itself against disaster. If a major storm hits, VG would likely bear part of the loss directly, compounding the revenue disruption with uninsured repair or replacement costs. This doesn’t seem to be risk management but risk retention.

Implications for LNG Export Financiers and Insurers

No one can predict the future. Over 80 bcm per year of LNG liquefaction capacity reached final investment decisions in the United States in 2025 – a new all-time high for the US LNG industry.121 The crisis in the Persian Gulf has rattled energy markets overnight. Like Russia’s invasion of Ukraine, this new war will likely supercharge short-term cash flows for US LNG exporters.

But financial actors should not mistake a geopolitical disruption for a durable change in market fundamentals or physical climate realities. The structural oversupply, litigation exposure and physical climate risks detailed in this brief represent medium- and long-term realities that will outlast any crisis-driven rally. Indeed, if exporters use current profits to accelerate expansion—as Venture Global’s aggressive growth strategy demonstrated above suggests they might—the eventual reckoning could be even more severe. And the LNG market could tank over the medium-term if energy importing countries conclude from the current conflict that LNG supply is just too unreliable and prices too volatile to plan around. Perhaps even more than Russia’s invasion of Ukraine in 2022, 2026 could prove to be the apex of irrational exuberance in the US LNG export market.

This brief explored how the rapid and highly-leveraged buildout of LNG export terminals along the US Gulf Coast carries significant equity, credit and insurance risks. The confluence of market, litigation, and physical climate risks described above creates compounding (and possibly under-priced) exposure for financial actors backing US Gulf LNG expansion.

For equity holders, Venture Global’s post-IPO collapse—losing over 60% of its value and roughly $37 billion in market cap122—signals that public markets are repricing the sector’s risk profile. As of Venture Global’s most recent annual disclosure in March 2026, alongside the arbitration proceedings detailed above, the company is defending itself against securities litigation filed by shareholders claiming that the company misled investors.123

For creditors, the LNG export sector’s heavy reliance on debt creates vulnerability if margins compress.124 Venture Global alone carries approximately $32 billion in debt,125 with a leverage ratio (an often-used measure of a company’s ability to pay off its incurred debt) above 14 and a long-term debt-to-equity ratio of 1031.126 This highly-leveraged capital structure assumes steady revenue from long-term contracts—but the company discloses that their customers may terminate these contracts under certain conditions.127 Meanwhile, the coming oversupply threatens to compress spot margins precisely when highly-leveraged operators need them most. As noted above, the Fitch and S&P downgrades following Venture Global’s arbitration loss demonstrate how quickly litigation risk can signal credit risk. Lenders face the prospect of borrowers squeezed simultaneously by weak spot prices, disputed contract revenue, and rising debt service costs.

For insurers, concentrated physical climate risk exposure in Cameron and Plaquemines Parishes—ranked #1 and #6 nationally for operational flooding risk—presents a growing structural problem which is only worsening with time.128 Venture Global’s disclosure that it relies on a captive insurance subsidiary for hurricane coverage129 suggests the traditional market is already pulling back. Earlier this month, maritime insurers chose to cancel war risk for LNG vessels in the Persian Gulf.130 Major insurers are already beginning to exclude coverage of LNG facilities in order to meet climate goals: Generali and Munich Re both have climate policies excluding LNG terminals from coverage.131 As climate losses mount across the US Gulf and geopolitical conflicts disrupt the Persian Gulf, insurers face a choice between repricing premiums to levels that erode project economics or exiting coverage entirely, leaving operators self-insured against billion-dollar disruption events.

These risks don’t operate in isolation. A major hurricane could simultaneously trigger insurance claims, disrupt revenue streams needed for debt service, spark contract disputes with offtakers over force majeure, and crater equity valuations—all while the broader market is oversupplied and margins are thin. Financial actors are not merely exposed to individual risks but to the interaction of each of them under stress.

LNG export along the US Gulf South poses untenable risks to coastal communities, to the climate, and to the very balance sheets of the financial actors supporting it.

Acknowledgements

This brief was written by Caleb Schwartz and Niko Lusiani. Much appreciation to useful feedback and contributions from Justin Mikulka from Oilfield Witness, as well as Shawna Ambrose, Ruth Breech, Toben Dilworth, Dianne Enriquez, Allison Fajans-Turner, Bree Flory, Ethan Nuss, and Aditi Sen at RAN.

Disclaimer

This publication is provided for informational and discussion purposes only and does not constitute investment, legal, tax, or other professional advice. While efforts have been made to ensure the accuracy and reliability of the information contained herein, no representation or warranty is made as to its completeness or suitability for any particular purpose. The authors and the Rainforest Action Network expressly disclaim any liability for any loss or damage arising from reliance on this publication. Readers should seek independent professional advice as appropriate.

Endnotes

- Methane gas, commonly referred to as “natural gas”, is primarily used as a fossil fuel to produce energy. This gas must be supercooled and liquefied in order to be shipped long distances. In its liquefied form, methane gas is commonly referred to as “liquefied natural gas,” or LNG. For more information: https://www.nrdc.org/stories/liquefied-natural-gas-101#industry

- https://www.woodmac.com/blogs/the-edge/war-is-once-again-reshaping-gas-and-lng/

- Kennedy, Seb. “War profits, quantified.” Energy Flux. March 4, 2026

- Kennedy, Seb. “War profits, quantified.” Energy Flux. March 4, 2026

- World Energy Outlook 2025. International Energy Agency, 2025, 72-73; see also section “Short-term LNG volatility cuts both ways” below.

- Williams-Derry, Clark, Mark Kalegha, Susan Torres, and Audrey Edwards. “North American LNG Export Tracker.” Institute for Energy Economics and Financial Analysis, January 2026.

- Gas 2025. International Energy Agency, 2025, 11.

- The CP2 LNG project reached final investment decision (FID) of $15.1 billion, Rio Grande Valley Train 4 received $6.7 billion, Rio Grande LNG Train 5 reached FID of $6.7 billion.

- Shiryaevskaya, Anna, Ruth Liao, and Stephen Stapczynski. “Global LNG Market Faces Looming Supply Glut After Years of Scarcity.” Bloomberg, September 7, 2025; Runciman, Josh. “Risks Mount as World Energy Outlook Confirms LNG Supply Glut Looms.” Institute for Energy Economics and Financial Analysis, November 15, 2024; S&P Global Energy. “Anticipated LNG Supply Glut Pushes Funds into EU Carbon Market.” November 24, 2025.

- Gas 2025. International Energy Agency, 2025, 6.

- Augusta, Alessandro. “How LNG Buyers Are Reshaping Global Gas Markets.” McKinsey & Company, February 2, 2026.

- World Energy Outlook 2025. International Energy Agency, 2025, 68.

- Alam, Shafiqul, Christopher Doleman, Haneea Isaad, et al. Global LNG Outlook 2024-2028. Institute for Energy Economics and Financial Analysis, 2024, 14.

- Global LNG Market Outlook 2030. Bloomberg, 3.

- Kramer, Kristy. “US LNG Expansion: Balancing Growth Ambitions with Oversupply Risks.” October 30, 2025.

- Bousso, Ron. “The US LNG Industry Risks Becoming Victim of Its Own Success.” September 22, 2025.

- Gas 2025. International Energy Agency, 2025, 6.

- Slocum, Tyson. “Exported Energy Affordability: How Trump’s Failed Energy Policy Is Driving America’s Energy Affordability Crisis.” Public Citizen, December 16, 2025.

- Struyven, Daan, Samantha Dart, Lina Thomas, Eoin Dinsmore, Yulia Zhestkova Grigsby, and Hongcen Wei. 2026 Outlook: Ride the Power Race and Supply Waves. Goldman Sachs, 2025.

- Alam, Shafiqul, Christopher Doleman, Haneea Isaad, et al. Global LNG Outlook 2024-2028. Institute for Energy Economics and Financial Analysis, 2024, 6.

- U.S. Energy Information Administration. “Europe’s LNG Import Capacity Set to Expand by One-Third by End of 2024.” November 28, 2022.

- Jaller-Makarewicz, Ana Maria. “EU Risks New Energy Dependence as US Could Supply 80% of Its LNG Imports by 2030.” Institute for Energy Economics and Financial Analysis, January 19, 2026.

- Institute for Energy Economics and Financial Analysis. “Europe’s LNG Buildout Slows amid Anticipated Decline in Gas Demand.” October 30, 2025.

- Gas Market Report, Q1-2026. International Energy Agency, 2026, 2.

- Institute for Energy Economics and Financial Analysis. “Europe’s LNG Buildout Slows amid Anticipated Decline in Gas Demand.” October 30, 2025.

- Hancock, Alice, and Rachel Millard. “Greenland Tensions Harden Europe’s Push for Energy Independence.” Financial Times, January 26, 2026.

- Ryan, Carol. “Europe Needs to Learn Its Lesson: Stop Relying on Imported Energy.” Wall Street Journal, February 11, 2026.

- International Energy Agency. “Japan – Natural Gas.” Accessed March 11, 2026.; International Energy Agency. “Korea – Natural Gas.” Accessed March 11, 2026.

- Alam, Shafiqul, Christopher Doleman, Haneea Isaad, et al. Global LNG Outlook 2024-2028. Institute for Energy Economics and Financial Analysis, 2024, 27-30.

- World Energy Outlook 2025. International Energy Agency, 2025, 71.

- Reynolds, Sam, and Christopher Doleman. “Japan’s Largest LNG Buyers Have a Surplus Problem.” March 11, 2024.

- Kim, Michelle, and Grant Hauber. “Prioritizing Economic Viability in South Korea’s U.S. LNG Import Strategy.” Institute for Energy Economics and Financial Analysis, June 23, 2025; Kim, Seoyoon. “Bridge to Nowhere: The Doomed Fate of Korea’s LNG Terminals.” Solutions for Our Climate. August 19, 2025.

- Gas 2025. International Energy Agency, 2025, 73.

- Alam, Shafiqul, Christopher Doleman, Haneea Isaad, et al. Global LNG Outlook 2024-2028. Institute for Energy Economics and Financial Analysis, 2024, 41.

- Varadhan, Sudarshan, and Emily Chow. “Philippines Unlikely to Add New LNG Terminal Near-Term on Excess Capacity.” Energy. Reuters, October 28, 2025.

- Reynolds, Sam, and Christopher Doleman. “Data Dive: The Drivers, Barriers, and Costs of Asia’s Gas and LNG Demand.” Institute for Energy Economics and Financial Analysis. Accessed March 5, 2026.

- Reynolds, Sam. “Global Gas Turbine Shortages Add to LNG Challenges in Vietnam and the Philippines.” Institute for Energy Economics and Financial Analysis, October 7, 2025.

- Reynolds, Sam. “Global Gas Turbine Shortages Add to LNG Challenges in Vietnam and the Philippines.” Institute for Energy Economics and Financial Analysis, October 7, 2025.

- World Energy Outlook 2025. International Energy Agency, 2025, 72.

- Xiong, Nelson. “China Gas Supply Strength Caps LNG Demand Growth.” Kpler, January 2, 2026; Nakano, Jane, and Leslie Palti-Guzman. “How the Power of Siberia 2 Deal Could Reshape Global Energy.” Center for Strategic and International Studies, September 5, 2025.

- Ong, Sing Yee, and Stephen Stapczynski. “Gas-Hungry Europe to Get Rare LNG Shipment Reloaded From China.” Bloomberg, February 12, 2026.

- Myllyvirta, Lauri, and Belinda Schaepe. “Analysis: Clean Energy Drove More than a Third of China’s GDP Growth in 2025.” Carbon Brief, February 5, 2026.

- Shi, Xunpeng, Belinda Schäpe, and Qi Qin. China’s Climate Transition Outlook 2025 Expert Survey. Center for Research on Energy and Clean Air, 2025, 4.

- Bloomberg News. “China’s Gas Growth to Slow as Cheaper Options Squeeze Demand.” Bloomberg, January 14, 2025.

- Reynolds, Sam. “Understanding the Competitive Landscape for China’s LNG Market.” Institute for Energy Economics and Financial Analysis, April 10, 2025.

- International Energy Agency. “Global Energy Review 2025: Electricity.” IEA, 2025

- Alam, Shafiqul, Christopher Doleman, Haneea Isaad, et al. Global LNG Outlook 2024-2028. Institute for Energy Economics and Financial Analysis, 2024.

- World Energy Outlook 2025. International Energy Agency, 2025, 70.

- World Energy Outlook 2025. International Energy Agency, 2025, 70.

- Agosta, Alessandro. “How LNG Buyers Are Reshaping Global Gas Markets” McKinsey & Company, February 2, 2026.

- Struyven, Daan, Samantha Dart, Lina Thomas, Eoin Dinsmore, Yulia Zhestkova Grigsby, and Hongcen Wei. 2026 Outlook: Ride the Power Race and Supply Waves. Goldman Sachs, 2025.

- Kennedy, Seb. “War profits, quantified.” Energy Flux. March 4, 2026

- Kennedy, Seb. “War profits, quantified.” Energy Flux. March 4, 2026

- World Energy Outlook 2025. International Energy Agency, 2025, 72-23.

- Alam, Shafiqul, Christopher Doleman, Haneea Isaad, et al. Global LNG Outlook 2024-2028. Institute for Energy Economics and Financial Analysis, 2024, 14

- SEC Form 10-K. Venture Global, Inc., 2026, 5.

- SEC Form 10-K. Venture Global, Inc., 2026, 5.

- Agosta, Alessandro. “How LNG Buyers Are Reshaping Global Gas Markets.” McKinsey & Company, February 2, 2026.

- Goh, Jeremy. “After the Storm: How Hurricanes Influence LNG Facilities and Natural Gas Hub Pricing.” Lexology, September 19, 2025; Bousso, Ron. “When the US Freezes, the Global LNG Market Catches a Cold.” Reuters, January 26, 2026.

- Global Energy Monitor Wiki. “Cameron LNG Terminal.” Accessed February 20, 2026.

- Duran, Mirza. “Cheniere, Sempra to Restart LNG Export Plants after Hurricane Laura.” LNG Prime, September 1, 2020; U.S. Energy Information Administration. “LNG Exports Resume from Sabine Pass and Cameron Terminals as Another Hurricane Approaches.” October 8, 2020.

- Goh, Jeremy. “After the Storm: How Hurricanes Influence LNG Facilities and Natural Gas Hub Pricing” Baker & O’Brien Inc., August 12, 2024.

- U.S. Energy Information Administration (EIA). “North America’s LNG Export Capacity Could More than Double by 2029.” October 16, 2025.

- U.S. Energy Information Administration (EIA). “North America’s LNG Export Capacity Could More than Double by 2029.” October 16, 2025.

- The 3rd National Risk Assessment: Infrastructure on the Brink. First Street Foundation, 2021.

- Sierra Club. “US LNG Export Tracker.” Accessed March 11, 2026.

- Authors’ estimates comparing EIA production capacity data to global LNG trade figures from the International Gas Union.

- Webster, Joseph, Reid l’Anson, and Anya Herzberg. “Hurricanes Could Upend US Oil and Gas Exports and Global Energy Markets. Here’s What to Know.” Atlantic Council, August 26, 2024.

- Lindsey, Rebecca. “Climate Change: Global Sea Level.” Climate.Gov, August 22, 2023.

- National Ocean Service. “NOAA Sea Level Trends.” Accessed March 5, 2026.

- Lee, Mike. “U.S. LNG Surge May Have a Flood Problem.” E&E News by POLITICO, June 8, 2022.

- Schmidt, Theresa. “Green Army General Russel Honore Takes on LNG Industry.” KPLC TV, August 24, 2022.

- Urgewald. “Global Oil & Gas Exit List.” Version 1.3. December 4, 2025.

- GlobalData. “Earnings Call Transcript: Venture Global’s Q2 2025 Results Show Strong Growth.” Investing.Com, August 13, 2025.

- “Venture Global.” Accessed March 11, 2026

- IEA (2026), Gas Market Report, Q1-2026, IEA, Paris, Licence: CC BY 4.0

- Venture Global. “Venture Global Announces Final Investment Decision and Financial Close for Phase 1 of CP2 LNG.” July 28, 2025.

- Venture Global. “Venture Global Announces Major Brownfield Expansion of Plaquemines LNG.” April 6, 2025. ; Venture Global. “CP3 LNG.” Accessed February 5, 2026.

- “Venture Global Reports Third Quarter 2025 Results.” November 10, 2025.

- Authors’ synthesis based on Venture Global: https://www.wsj.com/market-data/quotes/VG/financials (Accessed Feb 18, 2026); Cheniere Energy: http://www.wsj.com/market-data/quotes/LNG/financials (Accessed Feb 18, 2026); Sempra Energy: https://www.wsj.com/market-data/quotes/SRE/financials (Accessed Feb 18, 2026); data compiled by Bloomberg LP regarding companies under BICS category “Midstream – Oil and Gas”; data compiled by Bloomberg LP regarding investment-grade non-financial companies listed in the S&P 500 Index.

- Based on Venture Global’s $31.7 billion total long term net debt disclosed as of Sep. 30, 2025 (SEC 10-Q, page 8), Cheniere’s $22.7 billion long-term debt, net of unamortized discount and debt issuance costs as of Sep. 30, 2025 (SEC 8-K, page 11), Sempra’s $9.5 billion in projected proportionate net debt as of Dec 31, 2025 (Sempra Global), and NextDecade’s $6.6 billion in net debt as of Sep. 30, 2025 (SEC 10-Q, page 2)

- Levine, Matt. “Venture Global’s Gas Plant Is Done.” Bloomberg, October 14, 2025.

- Cocklin, Jamison. “Pressure Mounts Against Venture Global to Start Commercial Service on Time at Plaquemines LNG.” Natural Gas Intelligence, October 17, 2025.

- Levine, Matt. “Venture Global’s Gas Plant Is Done.” Bloomberg, October 14, 2025.

- “Fitch Revises Outlook on Venture Global to Negative; Affirms IDR at ‘B+.’” Rating Action Commentary. Fitch Ratings, October 15, 2025.

- “Fitch Revises Outlook on Venture Global to Negative; Affirms IDR at ‘B+.’” Rating Action Commentary. Fitch Ratings, October 15, 2025.

- SEC Form 10-K. Venture Global, Inc., 2026, 40.

- For example, Bowes v. Venture Global, Inc., No. 1:25-cv-01364 (S.D.N.Y.); Nikše, Dragana. “US LNG Player Faces Lawsuit for ‘Misleading’ Stock Buyers.” Offshore Energy, March 14, 2025.

- Jallal, Craig. “Calcasieu Pass commissioning cargoes dispute – no winners in sight.” Riviera Maritime Media, May 6, 2024.

- Morenne, Benoît, and Jenny Strasburg. “The U.S. Gas Startup at the Center of an Epic Feud With Global Energy Giants.” Business. Wall Street Journal, December 6, 2023.

- SEC Form 10-K. Venture Global, Inc., 2026, 12.

- Morenne, Benoît, and Jenny Strasburg. “The U.S. Gas Startup at the Center of an Epic Feud With Global Energy Giants.” Business. Wall Street Journal, December 6, 2023.

- SEC Form 10-K. Venture Global, Inc., 2026, 99-100.

- Shiryaevskaya, Anna. “Venture Global Confident It Will Win Other LNG Cases After Shell.” Bloomberg. August 13, 2025

- SEC Form 10-K. Venture Global, Inc., 2026, 100.

- SEC Form 10-K. Venture Global, Inc., 2026, 100.

- Glover, George. “Venture Global Stock Tumbles Almost 20%. It Just Lost This Bust Up With BP.” Barron’s, October 10, 2025.

- S&P Global. “Venture Global LNG Inc. Outlook Revised To Negative On Potential Impact Of Arbitration Ruling; ‘BB-’ Rating Affirmed.” October 16, 2025; “Fitch Revises Outlook on Venture Global to Negative; Affirms IDR at ‘B+.’” Rating Action Commentary. Fitch Ratings, October 15, 2025.

- Hernandez, America, and Curtis Williams. “Total CEO Says Company Rejected Venture Global as LNG Supplier over Lack of Trust.” Reuters, February 5, 2025.

- SEC Form 10-K. Venture Global, Inc., 2026, 99-100.

- SEC Form 10-K. Venture Global, Inc., 2026, 99-100. Landini, Francesca, Curtis Williams, and Arunima Kumar. “Venture Global Wins Arbitration Case Brought by Spain’s Repsol.” Reuters, January 22, 2026.

- SEC Form 10-K. Venture Global, Inc., 2026, 99-100.

- McKenna, Phil. “Fishermen in Southwest Louisiana Say LNG Terminals Are to Blame for Shrimp Harvest Decline.” Inside Climate News, September 7, 2025.

- Cunningham, Nicholas. “Dredge Operation near Venture Global’s CP2 Spills into Fish Habitat.” Gas Outlook, August 26, 2025.

- McKenna, Phil. “Fishermen in Southwest Louisiana Say LNG Terminals Are to Blame for Shrimp Harvest Decline.” Inside Climate News, September 7, 2025.

- Carby, Anissa. “Fishermen, Community Leaders Escorted out of International LNG Summit in Lake Charles.” KPLCTV, October 20, 2025; Muller, Wesley. “Shrimpers Join Environmentalists in Protest of LNG Terminal Expansions.” Louisiana Illuminator, November 10, 2022.

- Alexandra Shaykevich. Terminal Trouble. Environmental Integrity Project, 2025.

- Cavcic, Melisa. “Legal Setback for US LNG Arena: Court Nixes $11 Billion Gulf Coast Project’s Permit.” Offshore Energy, October 20, 2025.

- “Louisiana Fishermen, Communities, and Public Interest Organizations Ask D.C. Circuit to Halt Harmful Construction of Venture Global’s CP2 Export LNG Terminal and Pipeline.” Southern Environmental Law Center, September 8, 2025.

- Yoder, Naomi. “Plaquemines LNG Export Terminal, As Foolish as It Is Dangerous.” Healthy Gulf, September 13, 2021.

- Mufson, Steven, and Ricky Carioti. “A Rising Fortress in Sinking Land.” Washington Post, July 5, 2024.

- The 3rd National Risk Assessment: Infrastructure on the Brink. First Street Foundation, 2021.

- The 3rd National Risk Assessment: Infrastructure on the Brink. First Street Foundation, 2021.

- Porter, Jeremy, Evelyn Shu, Michael Amodeo, Ho Hsieh, Ziyan Chu, and Niel Freeman. “Community Flood Impacts and Infrastructure: Examining National Flood Impacts Using a High Precision Assessment Tool in the United States.” Water (Basel, Switzerland), November 5, 2021.

- SEC Form 10-K. Venture Global, Inc., 2026, 10.

- VG Balance Sheet. Wall Street Journal, (Accessed on Feb. 4, 2026)

- Brown, Taylor Kate. “Property Insurance Disappears for Louisianans – but Not for Gas Facilities.” Environment. The Guardian, July 24, 2023.

- Ainsworth, Bill, and Susan Milligan. “Climate Change Is Upending Homeowners Insurance Nationwide.” Institute for Business in Global Society, August 21, 2025.

- SEC Form 10-K. Venture Global, Inc., 2026, 43.

- SEC Form 10-K. Venture Global, Inc., 2026, 43.

- Gas Market Report, Q1-2026. International Energy Agency, 2026, 7.

- The IPO was priced at $25 per share in January 2025; current price is around $9.60, as of early February 2026.

- SEC Form 10-K. Venture Global, Inc., 2026, 98-99.

- “LNG Finance in World Markets.” Poten & Partners, October 22, 2025.

- “Venture Global Reports Third Quarter 2025 Results.” November 10, 2025.

- VG Financials. Wall Street Journal, (Accessed on Feb. 4, 2026)

- SEC Form 10-K. Venture Global, Inc., 2026, 8.

- The 3rd National Risk Assessment: Infrastructure on the Brink. First Street Foundation, 2021, 11.

- Form 10-K. Venture Global, Inc., 2026, 43.

- Shamim, Sarah. “Maritime Insurers Cancel War Risk Cover in Gulf: Will It Hike Energy Costs?” Al Jazeera, March 3, 2026.

- Munich Re’s approach to fossil fuels in investments and (re)insurance. Munich Re, 2025; Furness, Virginia. “Italy’s Largest Insurer Expands Oil and Gas Exclusions List.” October 22, 2024.